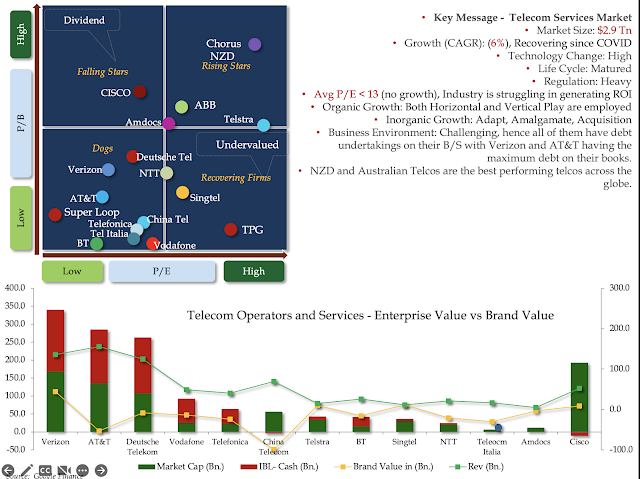

How Australian Telcos are Outperforming their Global Peers

Globally, telecom players are facing cut-throat competition from various players across Tier 1-3 operators and OTT players. Here in Australia, there is an Oligopoly of operators across fixed lines and mobile, hence services are expensive and they command better margins on their services.

Enterprise Value and Market Cap. of NBN in Jan 2023 - Without deferring the debt of $32 Bn.

- If NBN is sold today, it will get around $24 - $26 Bn, and that is less than what the Govt has infused as equity ($29.5 Bn).

Other Key Points:

- With the highest EBITDA Margin among the major Telecom Players in Australia, keen to know why the wholesale price can't be reduced, esp when Govt has deferred $32Bn in debt and, in effect, IBL is only for $12 Bn.

- With the change in direction of NBN rollout from Economies of Scope to Economies of Scale, NBN will benefit across the value chain. Benefits in terms of product rationalisation, workforce harmonisation, vendor consolidation, IT simplification, and more.

- IT will benefit from this shift by reducing the OPEX profile enabled by simplicity, standardisation of data, and boundary-less information flow. The new CIO has the depth and expertise in the IT and Telco domains to make this transition swiftly.

EBITDA Margin and Volatility of Stock

NBN has the maximum EBITDA Margin, and NTT has the least.

Operators with the least margin and with struggling operations will have declining OPEX dollars and will free up Cash for digital transformation dollars. Hence, the Vendors will target them.

Verizon and Telstra are the least volatile stocks, whereas NTT and CISCO are the most volatile. Stocks with less volatility are good candidates for dividend earnings and have stable market conditions, where long-term initiatives can be executed.

IT Services Opportunity in Telecom - 2023