IBM a Tech Giant - How it Lost its Way

Key Indicators

- Market Cap – $129.39Bn

- EV – $173.4Bn

- Debt - $57.5Bn, Cash - $17.9Bn

- P/B – 8.57

- P/E (Trailing) – 60.44 (Growth)

- P/E (Forward) – 14.3 (Div. Centric, No Growth)

- Economic Moat: Narrow (under threat)

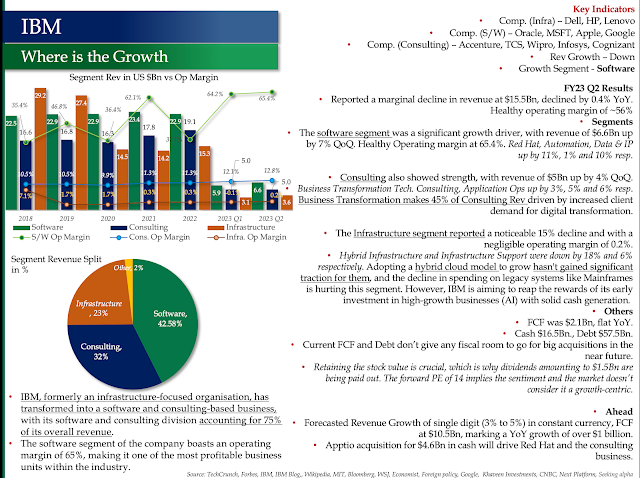

Where is the Growth

How it Lost its Way

- IBM a more than 100-year-old company that used to be a trendsetter in the technology space has become a laggard and is struggling to get its Mojo back. It is facing headwinds, and it is not clear how it will modernise its business. Today, IBM has 3 business segments, Infrastructure, Software and Consulting, and all of them are declining YoY. There are multiple reasons why IBM's revenues are declining except for the minor surge in 2021, and 2022. Let's look at the key reasons.

- Unlike its peer group players like Salesforce and ServiceNow which specialises in providing packaged application software in the Cloud (SaaS), IBM has no application software to offer. Instead, IBM's software offering is primarily in system software, such as middleware, database management systems, and operating systems, that are used to build applications, but it has no end-user applications to offer. To add further, the issue with IBM's system software business is that it is increasingly moving towards open-source software, like how its other peer, Oracle is facing headwinds in the Database domain. IBM's Red Hat Enterprise Linux is built on open source and is cheaper than the company's legacy proprietary software.

- Microsoft, it's another peer, that competes with IBM in the Enterprise IT, has developed a mousetrap around Windows OS and its MS Office offering for both consumers and businesses. IBM, on the other hand, has no such product. Its other distant peer group players like Google and Meta, unlike IBM, earn most of its revenue from advertising.

- The IT spending in OPEX has been flat since the augment of Digital Transformation in the early 2010s. Most of the IT spending is CAPEX-centric for corporates to transform their businesses by rolling out customer-centric applications in the cloud and reducing the spending on system upgrades like Mainframes. In a way, the IT spending profile has significantly changed from being OPEX and IT-centric to CAPEX and business-driven. To add further, the Cloud first approach by businesses got a boost during the pandemic for resiliency and agility, ensuring that the likes of AWS and Microsoft extended their market share. In comparison, IBM has been relegated to a Cloud Consulting business where they help implement AWS, Azure and Google Cloud for their clients. This change is validated by IBM's Cloud market share decline from 25% in 2016 to 4% in 2022, indicating a lack of success in its effort to be a major player in this segment.

- IBM ventured into the AI industry during the early 2010s, introducing its Watson platform. However, the platform's performance was lacklustre, resulting in IBM selling its Watson Health initiative at a significant loss. The company is now making a fresh push into the market by relaunching Watson with the new name of watsonx, keeping in mind the current trend of Generation AI. IBM had previously rebranded its flagship database from DB2 to Db2 to rejuvenate it, but the move led to its downfall, especially among developers. IBM is now attempting a similar strategy with its AI offerings. It remains to be seen, whether rebranding will help IBM boost its AI efforts and achieve much-needed growth.

- During the mid-1990s, IBM decided to shift its focus from hardware manufacturing to the IT Managed Infrastructure Services sector, to drive growth in its software and consulting businesses by moving up the value chain. This strategic transition was necessary to meet the changing needs of customers who were moving away from mainframes and towards commodity hardware-enabled servers. However, in recent years, the IT Managed Infrastructure Services industry has experienced a decline due to the emergence of Hyperscalers and a change in IT spending. Today, most of IBM's original mainframe customers have shifted to the cloud or on-premise commodity hardware platforms for new application development, adding to the company's current challenge of finding ways to drive growth.

- IBM's IT Consulting segment has maintained a steady performance, with operating margins staying flat at 10-12%. The company has been pushed by market forces to shift its focus from providing consulting services solely based on its products to helping clients implement software from other companies. This shift is similar to the approach of a System Integrator. Despite IBM's attempt to emulate the cost arbitrage model of the leading Indian SI players, it has not been successful. Additionally, the margins in the consulting business have decreased, whereas the software business provides healthy margins due to the negligible marginal cost of selling an additional unit.

- To summarise, It's unsurprising that IBM is undervalued in comparison to its peers, given the various aspects that have been discussed. Wall Street analysts view IBM as a dividend stock with limited potential for capital growth, which is reflected in its forward PE of 14 and the market cap of $129Bn only, 18 times less than Microsoft's market cap of $2.4Tn.

My other posts on Generative AI and Strategic Analysis of Key Players

- AI Value Chain

- Amazon the King of Retail -WhyAWS is the Crown Jewel

- Microsoft the King of AI in Software, Salesforce under the AI Cloud

- Tesla - It's not a Car, It's an AI Device on Wheels

- Google the King of Search - What the Future Beholds in the AI World

- Nvidia Godfather of AI - Why the Market is Bullish

- Generative AI can transform Telecoms, Energy and Utilities

Source: SeekingAlpha, Bloomberg, Martinfowler.com, Databricks.com, Nvidia, Google, AWS, Fourweek MBA Blog, Amazon, Ashwath Damodaran, TSMC