First, what I wrote about ABB's FY23 Results last year.

Update on ABB's Business

ABB's Acquisition Spree - Ongoing Tussle and Drivers Behind it.

My other post on NBN and its Economics

First, what I wrote about ABB's FY23 Results last year.

Update on ABB's Business

ABB's Acquisition Spree - Ongoing Tussle and Drivers Behind it.

Australia Telecom Industry in Transition - From Four Pillar to Six Pillar Model

My previous post on the Global Telecom Industry Evolution to date.

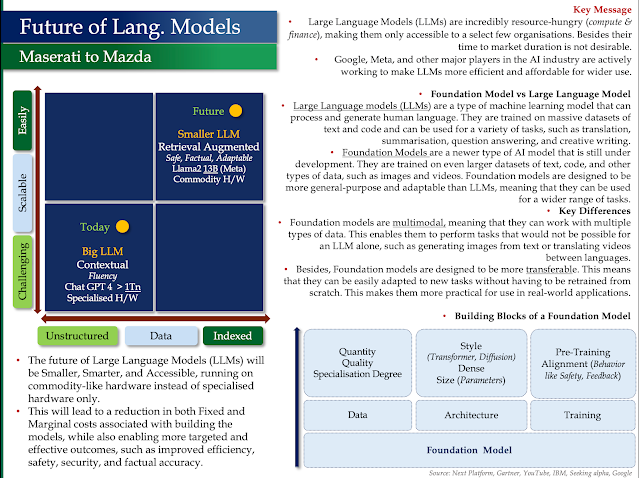

Future of Language Models

Foundation Model vs Large Language Model

Large Language models (LLMs) are a type of machine learning model that can process and generate human language. They are trained on massive datasets of text and code and can be used for a variety of tasks, such as translation, summarisation, question answering, and creative writing.

Foundation Models are a newer type of AI model that is still under development. They are trained on even larger datasets of text, code, and other types of data, such as images and videos. Foundation models are designed to be more general-purpose and adaptable than LLMs, meaning that they can be used for a wider range of tasks.

Key Differences

Foundation models are multimodal, meaning that they can work with multiple types of data. This enables them to perform tasks that would not be possible for an LLM alone, such as generating images from text or translating videos between languages.

Besides, Foundation models are designed to be more transferable. This means that they can be easily adapted to new tasks without having to be retrained from scratch. This makes them more practical for use in real-world applications.

Generative AI - Framework to Identify Use Case and Investment

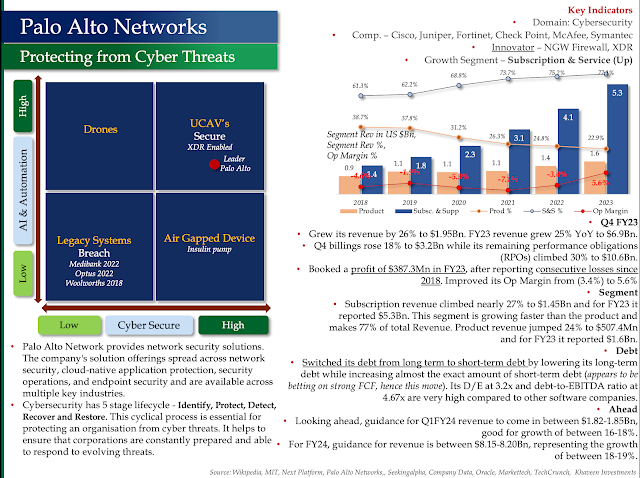

Key Indicators

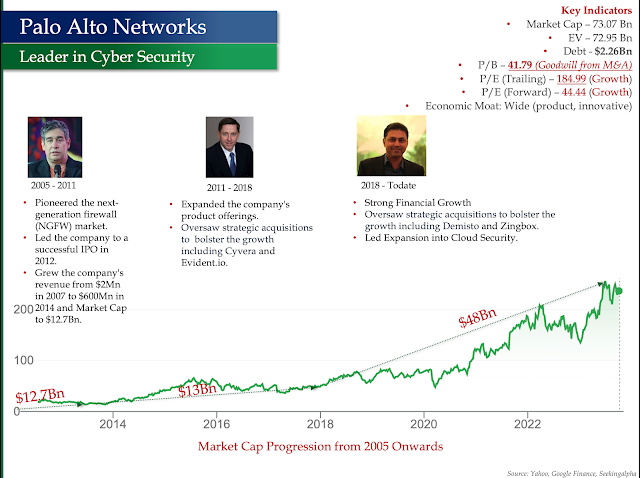

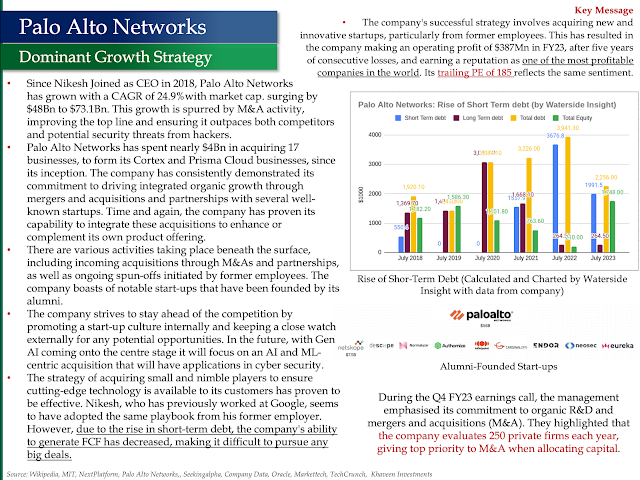

Since Nikesh Joined as CEO in 2018, Palo Alto Networks has grown with a CAGR of 24.9% with market cap. surging by $48Bn to $73.1Bn. This growth is spurred by M&A activity, improving the top line and ensuring it outpaces both competitors and potential security threats from hackers.

Palo Alto Networks has spent nearly $4Bn in acquiring 17 businesses, to form its Cortex and Prisma Cloud businesses, since its inception. The company has consistently demonstrated its commitment to driving integrated organic growth through mergers, acquisitions, and partnerships with several well-known startups. Time and again, the company has proven its capability to integrate these acquisitions to enhance or complement its own product offering.

There are various activities taking place beneath the surface, including incoming acquisitions through M&As and partnerships, as well as ongoing spin-offs initiated by former employees. The company boasts of notable start-ups that have been founded by its alumni.

The company strives to stay ahead of the competition by promoting a start-up culture internally and keeping a close watch externally for any potential opportunities. In the future, with Gen AI coming onto the centre stage it will focus on an AI and ML-centric acquisition that will have applications in cyber security.

The strategy of acquiring small and nimble players to ensure cutting-edge technology is available to its customers has proven effective. Nikesh, who has previously worked at Google, has adopted the same playbook from his former employer. However, due to the rise in short-term debt, the company's ability to generate FCF has decreased, making it difficult to pursue any big deals.

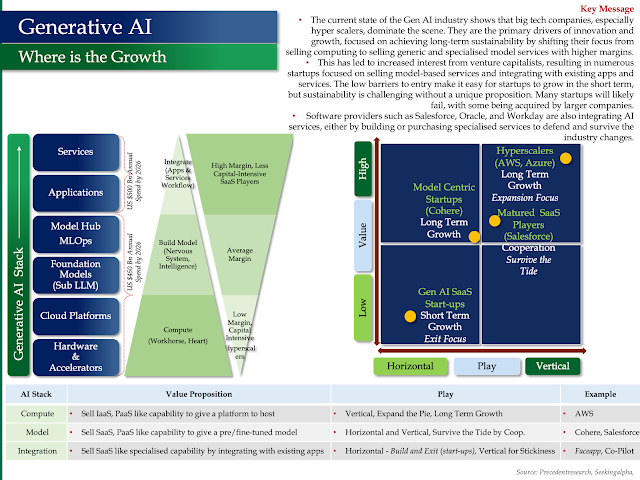

Generative AI - Changing the World, Key Players and Their Progress - Part One